Imagine opening your mail to find that the medication you’ve taken for years is suddenly more expensive-or worse, not covered at all. This isn’t a hypothetical nightmare; it’s the reality for millions of Americans navigating formulary updates. These are systematic changes made by insurance providers and pharmacy benefit managers (PBMs) that dictate which drugs are covered, at what cost, and under what conditions. If you rely on prescription medications, understanding these shifts is no longer optional-it’s essential for protecting your health and your wallet.

The Landscape of Prescription Drug Coverage in 2026

To understand where we are today, we have to look at how the system evolved. Since the inception of Medicare Part D in 2006, formulary management has been a balancing act between cost containment and patient access. However, the game changed significantly with the Inflation Reduction Act (IRA) of 2022. Signed into law by President Biden, this legislation fundamentally restructured how prescription drug plans operate. By January 1, 2025, most major changes took effect, setting the stage for the current environment in 2026.

The core value proposition for insurers remains cost control, but the mechanisms have shifted. For patients, the primary concern is maintaining uninterrupted access to necessary medications without facing unexpected financial burdens. According to an October 2024 analysis by AARP, the most significant patient-facing change was the implementation of a $2,000 annual out-of-pocket cap on prescription drug expenses. This cap benefits an estimated 3.2 million Medicare Part D enrollees, who save an average of $1,500 annually, with some saving $3,000 or more. While this is a relief, it doesn't eliminate the complexity of formulary tiers and exclusions.

How Formularies Are Structured: Tiers and Costs

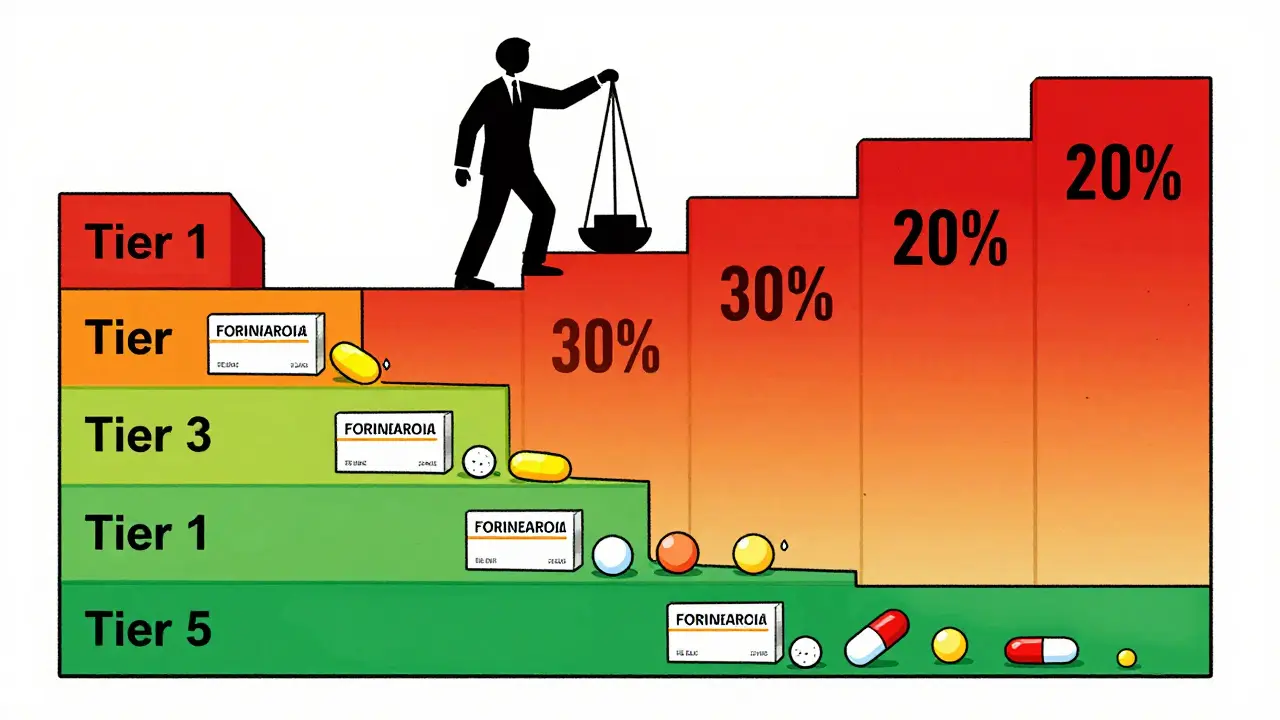

Formularies aren't just lists of drugs; they are tiered systems designed to influence prescribing behavior. Understanding these tiers is crucial because they directly impact your copay. Based on 2025 CMS data, which largely informs the 2026 landscape, the structure typically looks like this:

- Tier 1 (Preferred Generics): Lowest copays, averaging $1-$10. These are usually the most cost-effective options.

- Tier 2 (Non-Preferred Generics & Preferred Brands): Moderate copays, averaging around $47.

- Tier 3 (Non-Preferred Brands): Higher copays, averaging $113.

- Specialty Tier: High-cost medications, often requiring $113 or 25% coinsurance.

The IRA eliminated the coverage gap, commonly known as the "donut hole," and implemented the catastrophic phase at a lower threshold. This means that once you reach the initial coverage limit ($5,030 in 2025), you move into catastrophic coverage where costs are significantly reduced. However, getting to that point still requires navigating the lower tiers efficiently.

Generic Switching: The Push for Biosimilars

One of the most aggressive strategies employed by PBMs is generic switching, particularly the shift toward biosimilars. A biosimilar is a biological product highly similar to an FDA-approved reference product. Unlike small-molecule generics, biosimilars require complex manufacturing processes, but they offer substantial cost savings.

Milliman’s November 2024 analysis revealed a stark contrast in market approaches. Standalone Prescription Drug Plans (PDPs) are far more aggressive than Medicare Advantage Prescription Drug (MAPD) plans. In 2025, 78% of PDP formularies implemented substantial generic substitution policies, compared to only 42% in the MAPD market. CVS Caremark, for instance, excluded sixteen drugs in their 2025 update, including nine specialty medications, while adding eighteen new drugs to their standard coverage. Notably, they added oncology biosimilars Kanjinti and Trazimera, replacing Herzuma and Ogivri, which were excluded in 2024.

This trend is driven by regulatory shifts. The FDA’s May 2024 updated guidance on biosimilar interchangeability gave PBMs increased confidence to cover biosimilars even without the formal "interchangeable" designation. Dr. Sally Blount, Deputy Commissioner for Policy at the FDA, noted in June 2024 congressional testimony that this flexibility accelerates adoption. Consequently, biosimilar market penetration is projected to reach 45% for targeted therapies by 2027, up from 28% in 2024.

| Feature | PDP (Standalone) | MAPD (Medicare Advantage) |

|---|---|---|

| Generic Substitution Aggressiveness | High (78% implementation rate) | Moderate (42% implementation rate) |

| Specialty Drug Exclusions | More frequent | Less frequent |

| Biosimilar Adoption | Rapid integration | Slower integration |

The Impact on Patients: Stories from the Frontlines

Data tells one story, but patient experiences tell another. Feedback from Medicare.gov forums in October 2024 showed that 68% of 1,247 respondents expressed concern about formulary changes affecting their medications. Specifically, 42% were worried about diabetes medication changes. On Reddit’s r/Medicare community, user 'MedicareWarrior87' reported a jarring experience: "My copay jumped from $35 to $113 overnight for Humalog insulin after UnitedHealthcare moved it to a higher tier."

However, not all switches are negative. User 'ArthriticMom' on HealthUnlocked shared a positive outcome: "My switch from Humira to Amjevita (a biosimilar) saved me $450 monthly with no difference in effectiveness." This highlights the dual nature of generic switching: it can disrupt care if managed poorly, but it can also provide significant financial relief when clinically appropriate.

Despite these successes, non-medical switching-insurer-driven changes not based on medical necessity-has increased by 23% year-over-year, according to healthcare attorney Scott Glovsky’s October 2024 FAQ. This creates significant disruption for patients who must navigate exception processes to maintain their preferred medications.

Navigating Changes: Steps to Protect Your Coverage

You don’t have to accept formulary changes passively. Here’s how to proactively manage your prescription drug coverage:

- Review Notices Early: CMS mandates that insurers provide 60-day advance notice for formulary changes affecting existing medications. Exceptions exist for newly approved generics, which may only have 30 days’ notice. Check your mail and online portals between October and December each year.

- Understand the Exception Process: If your medication is excluded or moved to a higher tier, you can request a tiering exception. Standard requests are processed within 72 hours, while expedited requests for urgent needs are handled within 24 hours. In 2024, 82.3% of tiering exceptions were approved, but only 47.1% of exceptions for completely excluded drugs succeeded.

- Consult Your Pharmacist: Pharmacists are invaluable resources. They can identify therapeutic alternatives that may be covered on lower tiers. Cigna’s member survey from August 2024 revealed that 73% of members affected by formulary changes successfully obtained exceptions through their physicians, though 38% reported waiting 10-14 days for resolution.

- Leverage Transitional Supplies: Insurers like Aetna require members to receive written notification at least 30 days before changes take effect, with provision for a 30-day transitional supply. Use this time to secure a doctor’s note or file an exception.

Looking Ahead: The 2026 Outlook

As we move through 2026, the Medicare Drug Price Negotiation Program (MDPNP) becomes a critical factor. Starting January 1, 2026, all Part D formularies must cover negotiated drugs, including Stelara (ustekinumab), Prolia (denosumab), and Xolair (omalizumab). This mandatory coverage requirement represents a shift from voluntary inclusion to regulatory compulsion.

Furthermore, Milliman projects that 65% of 2026 formularies will implement mandatory generic substitution policies for all non-protected classes where biosimilars exist. Protected classes-such as antidepressants, antipsychotics, and HIV/AIDS treatments-are shielded from certain restrictions, ensuring continued access for vulnerable populations. However, for other categories, expect increased pressure to switch to generics or biosimilars.

J.P. Morgan’s Healthcare Analysts project that the IRA’s provisions will reduce Part D plan profitability by 18-22% through 2027. This financial pressure may lead to further formulary restrictions unless premium adjustments occur. Stay informed, review your coverage annually, and engage with your healthcare providers to ensure seamless transitions.

What is a formulary update?

A formulary update is a change to the list of prescription drugs covered by your insurance plan. It can involve adding new drugs, removing existing ones, or changing the cost-sharing tiers (copays) for specific medications. These updates typically occur annually, with notices sent in the fall for changes effective the following January.

Why are insurance companies pushing for generic switching?

Insurance companies and Pharmacy Benefit Managers (PBMs) push for generic switching to reduce costs. Generics and biosimilars are significantly cheaper than brand-name drugs. By encouraging or mandating switches, insurers can lower overall spending, which helps keep premiums stable and reduces out-of-pocket costs for patients in the long run, although individual transitions can sometimes cause short-term disruptions.

Can I appeal if my medication is removed from my formulary?

Yes, you can file a tiering exception or coverage determination appeal. You need a letter from your doctor stating why the specific medication is medically necessary and why alternatives won’t work. Standard appeals are processed within 72 hours, while expedited appeals for urgent needs are handled within 24 hours. In 2024, over 82% of tiering exceptions were approved.

What is the $2,000 out-of-pocket cap mentioned in the article?

The $2,000 out-of-pocket cap is a provision of the Inflation Reduction Act that limits how much Medicare Part D beneficiaries pay for prescription drugs in a calendar year. Once you reach this threshold, you enter the catastrophic phase where you pay little to nothing for covered drugs. This cap fully replaced the previous "donut hole" coverage gap starting in 2025.

Are biosimilars as effective as brand-name drugs?

Yes, biosimilars are required by the FDA to be highly similar to their reference products with no clinically meaningful differences in safety, purity, or potency. Many patients report no difference in effectiveness when switching from brands like Humira to biosimilars like Amjevita, often resulting in significant cost savings.

When should I review my formulary for changes?

You should review your formulary between October and December each year. Insurance companies send Summary of Benefits and Coverage documents during this period, detailing any changes effective January 1 of the following year. Proactive review allows you to address issues before they impact your medication access.